The $240,000 Breakthrough: Why Student Loan Bankruptcy Isn’t the Dead End It Used to Be

The “permanent debt” dogma is finally cracking. For decades, the legal and financial worlds have operated under the assumption that federal student loans are an inescapable life sentence, a unique class of debt that survives even the most scorched-earth bankruptcy filings. But a new “Fresh Start” narrative is emerging, proving that the supposed dead end of student loan relief is actually a door that—with the right key—can be unlocked.

A $240,000 Reset is Possible

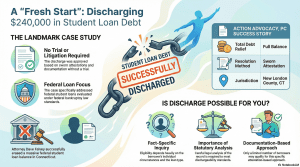

In January 2026, a legal milestone in New London County, Connecticut, fundamentally challenged the status quo of debt recovery. David Falvey, Esq., of Action Advocacy, PC, successfully secured the discharge of more than $240,000 in federal student loan debt for a single client.This isn’t just a win; it is a signal of a shifting tide. To ground this in reality, consider that $240,000 is nearly seven times the national average student loan balance. For the borrower in this case, that figure represented a mountain of debt that most would consider insurmountable. By clearing a quarter-million dollars in one stroke, this case proves that the “magnitude” of debt is no longer a disqualifier for relief, provided the legal groundwork is solid.

Bypassing the Courtroom Drama

What makes this breakthrough truly counter-intuitive is the procedural anomaly of its resolution: there was no adversary proceeding, no trial, and no contested hearing. Traditionally, seeking a student loan discharge required a borrower to engage in high-stakes litigation against the Department of Education—an expensive, emotionally draining “war room” scenario that discouraged all but the most desperate.Instead, this discharge was approved based on the “legal sufficiency of the record” presented to the court. By avoiding the traditional courtroom drama, this case demonstrates a streamlined path. It removes the primary barrier to entry—the fear of a long, costly legal battle—and suggests that the bankruptcy court is increasingly willing to find resolutions outside of a formal trial.

Letting the Documentation Speak for Itself

If the courtroom was the “where” they didn’t go, the “what” they used to win was a sophisticated evidentiary tool: the submission of a sworn attestation and supporting documentation. Rather than relying on oral arguments and cross-examinations, the legal strategy focused on creating an airtight paper trail that met federal standards.Regarding this mechanism, Attorney Dave Falvey noted:”This outcome reflects the importance of careful statutory analysis and the reality that some student loan debts may be dischargeable in bankruptcy depending on the specific facts and the type of loan involved.”This “careful statutory analysis” is the indispensable bridge between a borrower’s hardship and their freedom. It highlights that the “Fresh Start” isn’t granted through emotional pleas, but through the clinical application of federal law to a meticulously documented record.

Not All Debt is Created Equal

The significance of this case is heightened by the fact that it involved federal student loans. There is a common misconception that private student loans are the only ones susceptible to discharge, while federal loans remain “untouchable.” This case flips that script.By successfully navigating federal bankruptcy law standards for federal obligations, this outcome provides a roadmap for the very category of debt previously thought to be the most resilient. However, this distinction is a double-edged sword: borrowers must accurately identify their loan types (federal vs. private) before pursuing this path, as each requires a different legal maneuver.

The Path is Open, But It Isn’t Automatic

While we are entering a new era, a word of caution is necessary: this is not a “magic button” for debt elimination. Attorney Falvey is clear that student loan discharge is still difficult to obtain and remains a “highly fact-specific inquiry.” The “Fresh Start” is an option, but it is not an automatic right.Success in this arena depends on three rigid factors:

- The nature of the loans: Specific federal standards must be met.

- Individual circumstances: The borrower’s unique financial history and current hardship.

- Governing legal standards: The evolving interpretation of federal bankruptcy law.Because of these complexities, only a limited number of borrowers may currently qualify for this attestation-based approach. It requires a precise alignment of facts and a high level of documentation.

A New Era for Borrowers?

This Connecticut case marks a transformative moment for consumer bankruptcy and debt relief. It moves student loan discharge from the realm of “impossible” to “achievable for the prepared.” Action Advocacy, PC, based in Groton, continues to lead the charge in evaluating these federal options for those buried under debt.As the legal landscape shifts, the myth of “permanent” student debt is being dismantled one case at a time. If the “untouchable” nature of federal student debt is a thing of the past, what does that mean for your own path to financial freedom?

Action Advocacy, PC 1 Crouch St., Groton, CT 06340 860-449-1510 | [email protected] www.actionadvocacy.com