The 2026 Retirement Reckoning: 5 Impactful Realities of the UK’s New Pension Landscape

March 21, 2026 /Mpelembe Media/ — We are currently navigating a “demographic paradox” that threatens the very foundation of the British social contract. For decades, the logic of pension policy was simple: as we lived longer, we worked longer. But that trajectory has hit a wall. While the government continues to push retirement further into the horizon, our actual gains in longevity have begun to stall—and in some cases, retreat.April 2026 represents a “Triple-Uprating” stress test for the UK. It is the month where a new State Pension age phase-in, a CPI-linked benefit rise, and the “booster” effects of the Universal Credit Act 2025 all converge. As a strategist, I view this month not merely as a fiscal transition, but as a fundamental shift in responsibility from the State to the individual.Here are the five essential realities of the 2026/27 landscape that every worker and saver must navigate.

1. The 67 Trap: Why Your 66th Birthday is No Longer the Finish Line

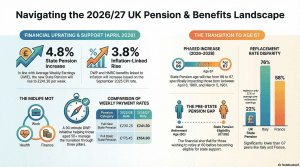

The era of retiring at 66 is officially coming to a close. Starting in April 2026, the UK begins a monthly “creeping” transition toward a State Pension age (SPA) of 67. This is not a sudden cliff-edge, but a phased delay that creates a complex eligibility calendar for those born in the 1960-61 window.The Phased State Pension Age Timetable (1960–1961 Cohort) If you were born during this period, your eligibility is calculated in “years plus months”:| Date of Birth Range | State Pension Age || —— | —— || 6 April 1960 – 5 May 1960 | 66 years, 1 month || 6 May 1960 – 5 June 1960 | 66 years, 2 months || 6 June 1960 – 5 July 1960 | 66 years, 3 months || 6 July 1960 – 5 August 1960 | 66 years, 4 months || 6 August 1960 – 5 September 1960 | 66 years, 5 months || 6 September 1960 – 5 October 1960 | 66 years, 6 months || 6 October 1960 – 5 November 1960 | 66 years, 7 months || 6 November 1960 – 5 December 1960 | 66 years, 8 months || 6 December 1960 – 5 January 1961 | 66 years, 9 months || 6 January 1961 – 5 February 1961 | 66 years, 10 months || 6 February 1961 – 5 March 1961 | 66 years, 11 months || 6 March 1961 onwards | 67th Birthday |

The Strategic Risk: The HLE Gap The real danger for workers isn’t just the age 67 threshold—it is the “Healthy Life Expectancy” (HLE) gap. While the SPA climbs to 67, the average UK HLE is now estimated at just age 63 . This creates a four-year “danger zone” where many will be too ill to work but too young to claim. Furthermore, longevity projections have been slashed; a newborn boy in 2050 was once expected to live to 95.5, but that has been revised down to 89.6. We are being asked to work longer for a retirement that is statistically shortening.Strategic Pivot: Do not rely on the State to bridge the gap between age 63 and 67. Use this period to maximize private “bridge” savings that can be accessed from age 57 to cover potential ill-health before the State Pension kicks in.

2. The G7 Abyss: The Individual Responsibility Shift

When compared to the world’s leading economies, the UK State Pension remains an international outlier in its lack of generosity. Data from Fidelity International and the OECD confirms that the UK occupies the bottom tier of the G7 regarding pre-retirement earnings replacement.| Country | Pre-Retirement Earnings Replacement Rate || —— | —— || Italy | 76% || France | 58% || UK | 22% |

In mainland Europe, the state pension is the “mainstay.” In the UK, it is designed strictly as a “foundation or top-up.” While total income often converges when private and occupational pensions are included, this represents a massive transfer of risk to the individual. Those who fail to save privately face a grim reality: the OECD 2022 estimate found that 14.5% of those aged 66 and over in the UK are already living in relative income poverty.As Marianna Hunt notes, the UK system functions as a “foundation or top-up,” making private provision not just a luxury, but a survival requirement.

3. The 2026/27 “Double Lift” vs. The Earnings Link

The financial year 2026/27 creates a stark divergence in how different groups are supported. Most inflation-linked benefits will rise by 3.8% (CPI). However, Universal Credit (UC) claimants will receive a significant “booster” via the Universal Credit Act 2025, which adds an additional 2.3% uplift.New Universal Credit Monthly Rates (2026/27):

- Single (Under 25): £338.58

- Single (25+): £424.90

- Joint (Both Under 25): £528.34

- Joint (Both 25+): £666.97Critically, the State Pension is set to rise by 4.8% , linked to Average Weekly Earnings (AWE). While the UC “double lift” is a welcome reprieve for the working-age population, it still trails the protected growth of the pension, reinforcing the widening gap between those in the workforce and those who have reached the exit.

4. The “Midlife MOT” Identity Crisis

To combat economic inactivity, the government has expanded the “Midlife MOT” to 40,000 in-person places. However, qualitative research reveals a program struggling with an identity crisis.

- The Branding Barrier: Many attendees find the “MOT” name “patronising,” suggesting that older workers are malfunctioning machinery in need of repair.

- The Digital Divide: While the DWP prioritizes digital links, attendees—many of whom manage their claims through younger relatives—are desperate for physical paper handouts.

- The Vulnerability Gap: Research shows the 90-minute group format is currently failing vulnerable groups. Those with learning disabilities or “very limited English” (ESOL) were observed struggling to understand the core concepts, indicating that “one-size-fits-all” is a failed strategy for the most at-risk.

- The Peer Effect: The most successful sessions were those where facilitators were pensioners themselves. These “peer messengers” could advocate for staying in work with a credibility that younger coaches lacked.

5. The Great Divergence: The Triple Lock Ratchet

Until the 1970s, the State Pension and unemployment support were siblings, tracking closely together. Today, they are strangers. Historical analysis from the House of Commons Library shows a “Great Divergence” driven by the “Triple Lock.”The Triple Lock has created a “ratchet effect”: every year it outpaces earnings, it increases the State Pension’s share of GDP. This makes SPA increases (like the move to 67) a mathematical necessity to “fund” the generosity shown to current retirees at the expense of the working-age population.”Uprating decisions and rules compound over time and have substantially changed the value of benefits, both in real terms and relative to earnings.”Strategic Pivot: Check your National Insurance record now. In a system where the “ratchet” makes every year of contribution count toward a 22% replacement rate, missing years are a luxury you cannot afford.

Conclusion: A Future Built on “Seeds”

The policy shifts of April 2026 are not just rows in a spreadsheet; they are, as Jobcentre staff describe them, the “planting of a seed” for a long-overdue conversation about financial resilience. The State is clearly signaling that its role is shrinking to that of a safety net, while the burden of prosperity in later life rests on individual shoulders.In a system where the State Pension is a “top-up” rather than a “mainstay,” and where the gap between being too ill to work and old enough to retire is widening, we must ask: Are we doing enough today to ensure our 67-year-old selves aren’t part of the 14.5% living in relative poverty? The time to bridge the gap is now, before the 2026 reckoning arrives.