From Copper to Gold: Zambia’s State-Led Blueprint for Formalizing Artisanal Mining

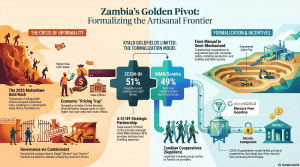

Wed, May 20 2026 /Mpelembe Media/ — Zambia is actively diversifying its mining economy beyond its traditional reliance on copper by executing a structural overhaul of its artisanal and small-scale gold mining (ASGM) sector. The primary catalyst for this shift was a massive, unregulated gold rush in the Kikonge area of Mufumbwe in mid-2025. The sudden influx of thousands of informal miners led to catastrophic safety failures, the emergence of illicit smuggling markets, and deadly clashes with state security forces. Recognizing that military intervention was an unsustainable fix for an economic problem, the Zambian government shifted toward a commercial integration strategy.

The centerpiece of this strategy is the incorporation of Kyalo Goldfields Limited (KGL), a joint venture between the state-owned ZCCM-IH (holding a 51% controlling stake) and the private, DRC-experienced operator Mining Mineral Resources (MMR). Rather than displacing local artisanal miners, KGL’s mandate is to organize them into legal cooperatives, replace dangerous hand-dug pits with semi-mechanized equipment, and build domestic refining infrastructure so the country can capture the lucrative downstream value of its gold.

This Zambian initiative reflects a broader African movement, spurred by record gold prices nearing $5,000 an ounce, to reclaim billions of dollars lost to informal smuggling corridors . A major hurdle in this effort is the “pricing trap,” where state buyers fail to match the high cash rates offered by tax-evading smugglers . Zambia aims to circumvent this trap by offering miners a superior value proposition: legal security, higher yields through better equipment, and a guaranteed market.

Furthermore, to ensure the gold meets international responsible sourcing standards, ZCCM-IH has partnered with the planetGOLD initiative to purchase gold from certified sites that eliminate the use of highly toxic mercury. Alongside KGL, the recent reopening of the previously troubled Kasenseli Gold Mine under a similar community-trust partnership signals Zambia’s comprehensive commitment to transforming volatile gold rushes into a formalized, state-anchored industry.

The $5,000 Ounce: How Africa’s Artisanal Gold Rush Went From “Side Hustle” to State Priority

When most people imagine the mining industry, they picture a clash of mechanized giants—titanic excavators and automated trucks carving out the earth using advanced hydrometallurgical extraction. Yet, for decades, a “shadow army” of millions has been doing this work by hand. Long dismissed as a marginal and largely informal “side hustle,” artisanal and small-scale gold mining (ASM) is currently undergoing a radical transformation into a cornerstone of national security and fiscal policy.The catalyst is a fundamental shift in global commodity valuations. With gold prices hovering near $5,000 per ounce following a staggering 70% surge in 2025, African governments have reached a tipping point. They can no longer afford to ignore the millions of individual miners operating within their borders. What was once a regulatory afterthought has become an urgent state priority.

Takeaway #1: The “Ignore-ance” Tax—Why Governments Can No Longer Look Away

Historically, artisanal mining was treated as a chaotic domestic challenge with negligible contributions to national treasuries. That narrative was shattered by the economic data of 2025. In Ghana, the continent’s top producer, the formalization of artisanal gold trading has yielded massive dividends. In 2025, the country exported approximately 100 tons of artisanal gold, generating $10 billion in revenue—nearly half of the nation’s total gold export earnings.However, a structural “Tax Imbalance” persists because tax systems for small-scale miners are often separate from those applied to industrial mines and remain notoriously difficult to enforce. According to the Ghana Chamber of Mines, while artisanal operations produced over 3 million ounces of gold in 2025, their direct tax contribution was less than 500,000 Ghanaian cedis. In stark contrast, industrial giants paid approximately 19 billion cedis.”Artisanal gold mining, long dismissed as a marginal and largely informal activity across Africa, is becoming one of the continent’s fastest-growing mining sectors as record gold prices reshape government policy and export strategies.”

Takeaway #2: The Mufumbwe Lesson—From Chaos to Corporate Architecture

The transition from unregulated chaos to state-led integration is best illustrated by the 2025 crisis in Zambia’s Mufumbwe District. An unregulated gold rush in the Kikonge area led to a catastrophic slope failure in June 2025 that killed six miners. By July, the “Swahiri” and “Ukraine” informal markets—hubs for untaxed trade and illicit goods—became the flashpoints for violent security clashes between police and miners, resulting in at least three confirmed deaths.Zambian authorities recognized that security-led containment was a fiscally draining failure. On May 6, 2026, the government pivoted toward “Corporate Architecture” with the incorporation of Kyalo Goldfields Limited (KGL) . This Special Purpose Vehicle is a joint venture where the state-backed ZCCM Investments Holdings (ZCCM-IH) holds a 51% majority stake, while Mining Mineral Resources (MMR) , a subsidiary of the Somika Group (Vinmart Group) , holds 49%.This structure is a sophisticated maneuver under the Minerals Regulation Commission Act No. 14 of 2024 . By maintaining a 51% stake, the state bypasses statutory reservation thresholds that typically restrict mid-scale mining rights to citizen-owned companies. Operationally, the partnership allows the state to leverage Somika’s technical expertise to move from dangerous, narrow hand-dug shafts to stabilized, engineered open-pit configurations.

Takeaway #3: The “Pricing Trap”—Why Smugglers Often Outbid States

Establishing state-backed buying offices is only half the battle; the “pricing trap” remains the primary hurdle to formalization. Smugglers, who evade export duties and corporate taxes, frequently offer higher cash rates than official state entities.

- Burkina Faso’s Success: By connecting certified cooperatives to buyers, the state helped official artisanal output jump to 42 tons in 2025.

- The DRC’s Struggle: Despite a target of 15 tons, the DRC’s state-owned trading company exported only 1.75 tons in 2024 due to uncompetitive official prices.To defeat entrenched smuggling networks, an expert analyst looks beyond the price tag. The state must provide a superior “Value Proposition”: providing geological data, access to semi-mechanized equipment, and guaranteed legal tenure. By increasing the total yield per ton and eliminating the risk of arrest, the state makes the black market economically uncompetitive.

Takeaway #4: “Green Gold” is the New Market Requirement

Formalization is also an environmental imperative. In Zambia, the planetGOLD initiative is working with 11,000 miners to align with the Minamata Convention on Mercury , which the nation ratified in 2016. The program aims to reduce mercury use by 1.14 metric tons over five years by introducing mercury-free technologies like “gold kachas, gold cubes, and blue bowls.”This “Green Gold” is no longer a luxury; it is a prerequisite for entering premium international markets in Europe and North America. To meet these standards, the sector is adopting the Five Pillars of Responsible Sourcing (based on the OECD framework):

- Management Systems: Establishing strong internal oversight and chain of custody.

- Risk Identification: Assessing the supply chain for conflict and human rights abuses.

- Risk Response: Designing strategies to mitigate identified threats.

- Third-Party Audits: Ensuring independent verification of mining sites and refineries.

- Public Reporting: Providing transparent annual disclosures on due diligence.

Takeaway #5: Gold as the New Global Reserve Strategy

Central banks in Ghana, Zimbabwe, and the DRC are now using artisanal production as a critical monetary tool to build national reserves. Evidence of this “in-country” value retention strategy is seen in the DRC’s pilot refinery in Kalemie, which boasts a capacity of 500–600 kg per month.The regional power dynamics are shifting: a firm within the same Somika/MMR conglomerate that partners with Zambia in KGL was also a foundational player in launching that DRC refinery in March 2026. Under the leadership of ZCCM-IH CEO Kakenenwa Muyangwa , Zambia is similarly pursuing a “royalty-to-revenue” model. By refining gold locally and capturing the premium spread, these nations are moving from passive observers of their mineral wealth to active commercial participants.

Conclusion: A Provocative Gaze Forward

The tools for transparency—traceability, digital monitoring, and real-time data—now exist and are being deployed at an unprecedented scale. The artisanal sector has shed its image as a marginal “side hustle” and taken its place as a cornerstone of national economic strategy across Africa.However, the speed of the black market remains the ultimate variable. Can African governments move fast enough to turn a volatile mineral rush into a stable national industry, or will the allure of unregulated trade always stay one step ahead of the law?