Philippe Burger, University of the Free State

Public debt repayments in some African countries are at their highest levels since 1998. The Conversation Africa’s founding editor Caroline Southey talks to dean and economics professor Philippe Burger about the danger of debt problems some African countries face.

What’s behind the spike in debt servicing repayments?

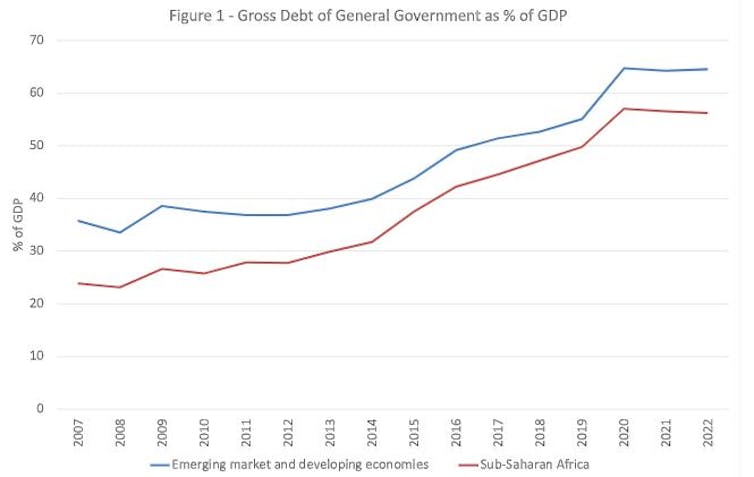

For most countries experiencing new highs in debt servicing costs, it is not so much a spike, but rather a gradual increase over several years. As Figure 1 which uses data from the International Monetary Fund (IMF) shows, the Gross Debt of General Government (which includes central, provincial/state, and local government levels) steadily increased as percentage of GDP over the last 15 years (for brevity we will call this ratio the debt ratio). This period includes the global financial crisis as well as the COVID periods.

For emerging market and developing economies the debt ratio increased from 33.5% in 2008 to 64.6% in 2022.

Though at a slightly lower level, the same scenario played itself out for sub-Saharan African countries. With higher debt comes higher debt servicing costs. Although the COVID pandemic caused an accelerated increase in the debt ratio, the ratio was on an upward trajectory well before the pandemic.

IMF, World Economic Outlook (for some countries 2022 is an estimate)

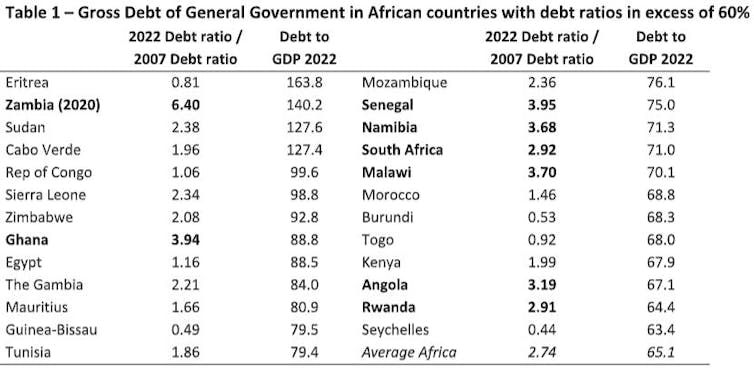

This trajectory can also be seen in individual countries. In Zambia the debt ratio was a mere 21.9% in 2007, but increased to 140.2% in 2020, when the government defaulted. In Ghana it was 22.6% in 2007, before quadrupling to 88.8% in 2022. The increase in the debt ratios in Zambia and Ghana can also be seen in the increase in their governments’ interest payments as percentage of GDP. In the case of Ghana, it increased from 1.4% in 2007 to 7.2% in 2022, while in Zambia it increased from 1.4% to 6%.

Ghana and Zambia have defaulted: what impact will this have?

A default often has a significant fallout in the economy, with governments, companies and households facing forced austerity. Governments must then cut back significantly on their expenditure, often in the face of shrinking tax revenues.

This often negatively affects social expenditure on for instance health and education. If such a country must knock on the door of the IMF for assistance, as both Ghana and Zambia had to do, the institution usually prescribes several tough policy and economic adjustments.

In early 2023 eleven of the top-20 borrowers from the IMF were African countries.

Egypt is the second largest borrower from the IMF, incurring loans in the aftermath of the political and economic instability that followed the Arab Spring in 2011.

The period leading up to a default is also often characterised by companies and households facing much higher inflation. This inflation often originates from a deep depreciation of the local currency because of capital flight of foreign and domestic investors losing confidence.

Both the Ghanaian Cedi and Zambian Kwacha depreciated significantly in the period leading up to their government’s default.

Which other African countries are on the watchlist: what stress signs should we be alive to?

Which countries to watch is a complex question. Although economists sometimes use rules of thumb, such as a debt ratio that exceeds say 60% or 90%, the answer depends on several variables. Thus, a high debt ratio is not always considered a problem.

For instance, at 121.7%, the debt ratio of the US is much higher than that of Ghana. Yet Ghana defaulted because the interest cost of its debt as percentage of GDP was much higher than that of the US (2.1% for the US).

In addition to the level of the debt ratio, the variables used to populate a watch list also include the rate at which the ratio changed over say 10 or 15 years, and closely related to that, the level and change in the size of the government’s borrowing.

Also included are the level and size of the governments primary balance (which is the deficit excluding interest payments and receipts), the interest cost on its debt, and the rate at which that cost changes.

Take the case of Zambia. Its debt ratio increased from 21.9% in 2007 to 140.2% in 2020, thus 6.4 times its 2007 level (see Table 1). At the same time its government annual borrowing increased from 1.04% of GDP in 2007 to 13.8% in 2020. The government’s primary balance deteriorated from a primary surplus of 0.34% of GDP in 2007 to a primary deficit of 7.8% in 2020. This also meant, as mentioned above, that its interest payments increased from 1.4% of GDP to 6% of GDP.

Whereas interest cost on government debt as percentage of GDP topped 6.3% in Zambia in 2020 and 7.2% in Ghana in 2022, no other African country with the exception of Egypt at 6.2% had an interest cost over 5% of GDP in 2022. Hence, most countries were in a fiscally healthier position than Ghana, Zambia and Egypt.

The debt ratios in Eritrea, Sudan, Cabo Verde, Republic of Congo, Sierra Leone, and Zimbabwe are all higher than Zambia’s at the time of its default (see Table 1). However, unlike Zambia and Ghana, their debt ratios did not increase as fast as either Zambia or Ghana (their 2022 debt ratios were between 0.81 and 2.38 times as high as in 2007 – also see Table 1).

IMF (2023a) World Economic Outlook (2022 values are IMF estimates) and author’s calculations

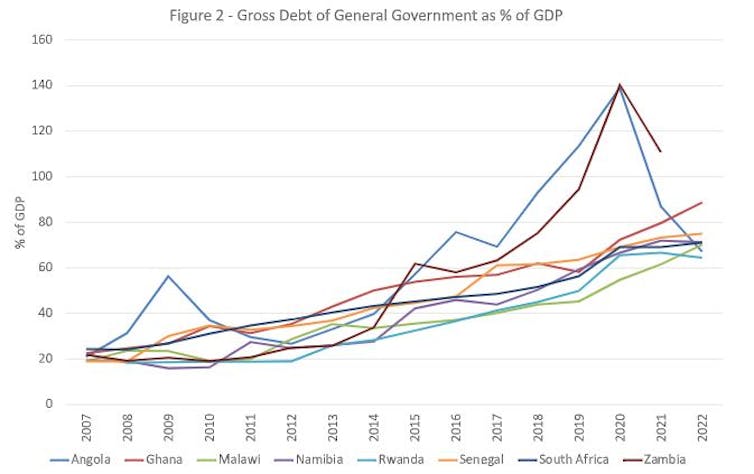

And while the 2022 debt ratios in Senegal, Namibia, Malawi, and Angola are three to four times what it was in 2007, the debt ratios are not yet as high as that in Ghana and Zambia.

In Angola the debt ratio is also falling significantly following a steep increase in the ratio in the preceding decade (see Figure 2). This was largely due to higher oil revenues and an appreciation of its currency that reduced the domestic currency value of its foreign-denominated debt.

IMF, World Economic Outlook (2022 values are IMF estimates)

Two further countries that need to tighten up their fiscal policies are Rwanda and South Africa, which both saw their debt ratios almost triple between 2007 and 2022.

Thus, although the debt situation in no African country is as bleak as the situation in Ghana and Zambia was at the time of their defaults, the situation in several countries is still not rosy.

Is debt forgiveness a possible solution?

Forgiveness can occur before or after default.

Let’s first consider forgiveness before default. Two decades ago, domestic debt markets in low- and middle-income countries were underdeveloped, and their governments depended on access to international financial markets to finance their debt. Debt forgiveness thus largely entailed foreign investors (often in advanced economies) taking a voluntary loss on their investments. This has changed.

Today domestic financial markets, in which local pension and insurance funds invest, play a much bigger role in the financing of government debt in low- and middle-income countries.

Forgiveness before default will therefore entail domestic investors taking voluntary losses on their investments to reduce the future tax liability that domestic debt implies for domestic taxpayers. Given that domestic pension funds also represent low-income members, the distributional effect of debt

forgiveness is not necessarily progressive (meaning that higher income earners do not necessarily carry the bulk of the burden in the event of forgiveness). Thus, forgiveness of domestic debt is probably a political non-starter.

Of course, in the event of a default, when debt is restructured, investors, including domestic investors, might have to accept haircuts (losses) or reduced returns on their investments. That would be involuntary forgiveness.

In addition, forgiveness may reduce the debt ratio, but it does not necessarily eradicate the initial mismatch between government revenue and expenditure that gave rise to the increasing debt ratio. It might even worsen the problem, because having debt forgiven once gives rise to the expectation that it will be forgiven again.

Forgiveness can thus give rise to a moral hazard problem and lead to a government becoming fiscally less prudent. Fiscal history is replete with countries that are serial defaulters.

Take-aways

The data show that the increased interest burden that some African countries face results from years of steadily rising debt ratios. And while Ghana and Zambia might have been the most serious cases, there are several other countries that can be placed on a “watch list”. To prevent a fiscal crisis, the governments in these countries will need to take steps to stimulate economic growth and reign in their public finances to arrest the steady, ongoing rise in their debt ratios.

Philippe Burger, Dean: Faculty of Economic and Management Sciences, and Professor of Economics, University of the Free State

This article is republished from The Conversation under a Creative Commons license. Read the original article.