Defending the Rails: How Mastercard’s Multi-Token Network is Countering the $27 Trillion Stablecoin Threat

The End of the “Wild West”: 5 Ways the Global Money Game Is Being Rewired

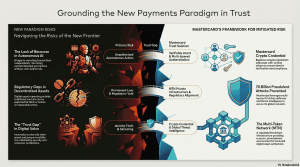

We live in an age of digital instantaneity. We can stream high-definition video from across the globe or summon a ride to our doorstep in seconds. Yet, when it comes to the movement of value, we often find ourselves tethered to a legacy “multi-day” financial settlement system—a relic of the analog age. This gap between our instant digital lives and the friction of modern money is finally closing.The 2026 payments landscape reveals a profound shift: the era of speculative “Wild West” crypto is giving way to a regulated, programmable economy. Mastercard is no longer merely a “card company”; it has pivoted to become the connective trust layer for a new paradigm of agentic commerce and tokenized value. By solving the “trust gap” that kept blockchain on the periphery for a decade, Mastercard is effectively institutionalizing the decentralized world. Here are the five most significant takeaways from this invisible revolution.

1. Your AI Assistant is Getting its Own Wallet (Agentic Commerce)

The most transformative shift in the digital economy is the rise of agentic commerce . In this model, Artificial Intelligence moves from a simple recommendation engine to an authorized transactional participant. We are moving beyond humans tapping screens; we are entering a world where AI agents execute payments autonomously, responding to context and intent.For this to work, the underlying plumbing must change. Traditional banking operates on “business hours,” but AI agents require 24/7/365 settlement —a need that Mastercard’s Multi-Token Network (MTN) is uniquely positioned to fill. To support this, the Mastercard Virtual C-Suite now provides small businesses with AI-powered experts in finance (Virtual CFO), marketing, and security to manage cash flow and invoices with superhuman efficiency.”Transactions are no longer just initiated by humans tapping a screen. They are initiated by authorized intelligent systems operating continuously, responding to context, preferences and intent. For this to work at scale, trust is essential.” — Jorn Lambert, Chief Product Officer, MastercardTo ensure security, initiatives like Agent Pay and Verifiable Intent act as guardrails. These frameworks allow users to define clear permissions, ensuring that even as agents operate autonomously, the human remains the ultimate authority in a secure audit trail.

2. The Death of the 42-Character Hexadecimal Address

For years, the psychological barrier to digital asset adoption was the “fat-finger” error. Sending money required navigating 42-character hexadecimal blockchain addresses where a single mistake led to irreversible loss.The Mastercard Crypto Credential is dismantling this barrier by replacing complex strings with human-readable aliases, such as ” alex.mastercard .” This system mirrors the simplicity of a Venmo handle while maintaining enterprise-level KYC and AML compliance.Crucially, the system introduces a “pre-facto” check mechanism . Through partnerships with Polygon Labs and Mercuryo , the network utilizes Soulbound tokens —non-transferable digital assets linked to a user’s identity—to verify credentials before the money moves. This prevents funds from being sent to incompatible wallets or, more importantly, to entities in sanctioned nations. By blocking the transaction before it is ever committed to the ledger, Mastercard provides a level of security previously absent from the self-custody ecosystem.

3. The Institutional Capture of Decentralized Liquidity

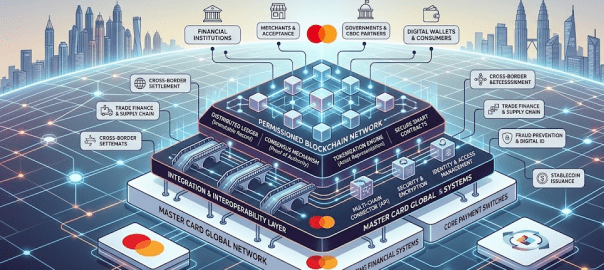

Mastercard is not seeking to replace the crypto ecosystem; it is positioning itself as the vital middleware that makes it usable for the masses. Through its Crypto Partner Program , Mastercard has built a coalition of over 85 firms, including Circle, Binance, Ripple, Gemini, and Paxos .This “Network Overlay” model wraps the “unsexy” trust infrastructure—dispute resolution, fraud protection, and chargebacks—around blockchain’s efficiency. The velocity of this shift is staggering: stablecoin payments hit $390 billion in 2025, representing a 673% year-over-year growth. Within that figure, B2B stablecoin payments alone reached ****$ 226 billion annually. Mastercard is capturing these flows by leveraging a network of 3.5 billion cardholders and 150 million merchants.”The real reason Visa and Mastercard can remain dominant isn’t about speed or cost, but trust and familiarity… Stablecoins excel at settlement but they lack the consumer protections and credit features that users have come to rely on.” — FinTech Weekly

4. Tokenizing the “Real World” (Beyond Currency)

The Multi-Token Network (MTN) represents Mastercard’s expansion into Real-World Assets (RWAs) . This private blockchain infrastructure brings 24/7 liquidity to traditionally illiquid markets by representing tangible and financial assets as digital tokens.Key proof points for the MTN’s expansion include:

- Tokenized Commercial Bank Deposits: Utilized by institutions like JPMorgan Kinexys and Standard Chartered for interbank settlement, providing atomic finality with zero counterparty risk.

- Tokenized Carbon Credits: Enabling transparent, auditable ESG tracking for global sustainability programs.

- Tokenized US Treasury Tokens: Facilitated via Ondo Finance (specifically their OUSG assets), allowing corporations to earn yield on treasury assets with the flexibility of on-chain liquidity.By moving these assets onto the MTN, Mastercard allows for real-time payments and redemptions, bypassing the congestion of public chains while utilizing Mastercard Move for seamless cross-border flows.

5. The Yield Hypocrisy—Protecting the “Low-Yield Moat”

A significant friction point has emerged in the form of the CLARITY Act debate. Traditional banks have lobbied aggressively to prohibit crypto platforms from offering yield or rewards on stablecoin holdings. They argue this is a safety issue, citing a theoretical $6.6 trillion in “at-risk” deposits that could flee community banks.However, a “yield hypocrisy” is evident. While banks lobby against these rewards, they simultaneously facilitate them through existing card rails. For instance, the Gemini Mastercard already offers 4% back in crypto on gas and transit. Analysts like Patrick Witt of the President’s Council of Advisors for Digital Assets point out that the predicted “deposit flight” has not manifested despite these rewards being available for years. This suggests the lobbying is less about systemic safety and more about maintaining a “low-yield moat” against more competitive financial entrants. Attempts to block these high-velocity rewards are increasingly viewed as anti-competitive measures designed to insulate legacy banking from the programmable reality of modern finance.

Conclusion: The Integrated Future

The global financial system is no longer split between TradFi and Crypto; it is converging into a single “programmable reality.” The invisible revolution is not just about the speed of money, but about the standards and plumbing that make that speed safe.Mastercard’s scale is the ultimate defense: the company has declined 70 billion fraudulent transactions over the last decade, a level of protection that pure decentralized protocols cannot yet replicate. As we integrate AI agents and tokenized treasuries into our daily routines, the technology under the hood will become invisible.When your AI agent can manage your cash flow and your morning coffee is paid for via a tokenized treasury, will you even care what “rail” the money traveled on—or will you only care that you can trust the transaction?